News List

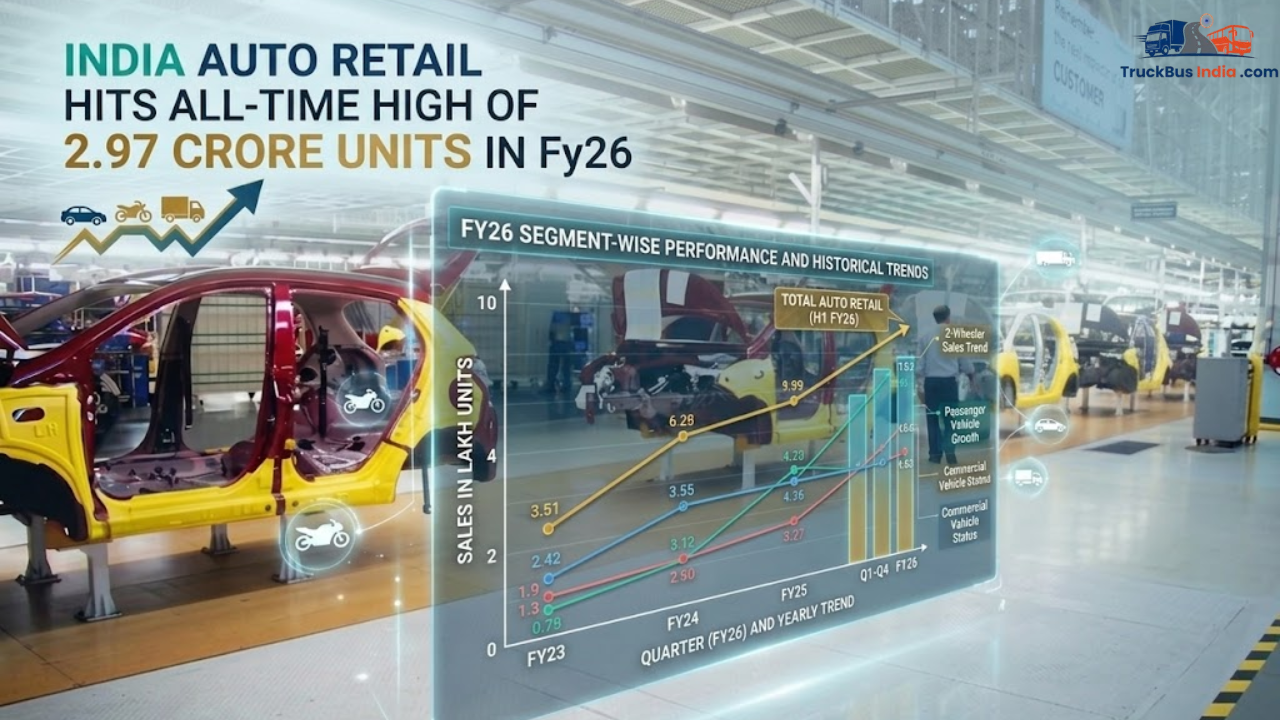

India Auto Retail Market Crosses Historic 2.97 Crore Units in FY26

India’s automobile retail sector closed FY 2025-26 at an all-time high of 2,96,71,064 units, marking a 13.30% year-on-year (YoY) growth and bringing the market close to the 3-crore milestone. Five of six vehicle categories achieved record annual sales, with only construction equipment showing a decline.

FY26: A Tale of Two Halves

The year started with muted growth of 2-5% monthly from April to August, as consumers adopted a wait-and-watch approach ahead of anticipated GST 2.0 reforms. Growth surged from September after revised GST rates reduced effective tax burdens on mass-segment two-wheelers, small cars, three-wheelers, and select commercial vehicles.

FADA President C S Vigneshwar described FY26 as “a landmark year for Indian auto retail,” crediting structural demand driven by rising affordability, expanding mobility across urban and rural India, and a diversifying powertrain mix.

The festive period was especially strong, with October recording over 40 lakh units. The momentum extended through January, February, and March 2026, confirming that growth was structural rather than seasonal.

Category-Wise Performance

- Two-Wheelers: Retail reached 2,14,20,386 units (+13.40%), reclaiming pre-COVID peaks. March alone saw 19,51,006 units (+28.68%).

- Passenger Vehicles (PVs): Crossed 47 lakh units (+13.00%) for the first time, supported by SUVs, alternative powertrains, and normalised inventory levels.

- Tractors: Historic milestone of 10,50,077 units (+18.95%), powered by a strong monsoon, robust rabi sowing, and improving farm economics.

- Commercial Vehicles (CVs): Surpassed 10 lakh units (+11.74%), with the MCV sub-segment up 25.50% in March.

- Three-Wheelers: 13,63,412 units (+11.68%), with EVs accounting for over 60% of retail.

- Construction Equipment: Only declining segment, down 11.70% to 71,227 units due to project delays and high base effects.

Powertrain Transition Accelerates

The EV and CNG adoption highlights the structural shift in India’s mobility landscape:

- Three-Wheelers: EV share reached 60.95%

- PV CNG Share: 21.98% (up from 19.60%), PV EV share 4.25% (up from 2.61%)

- Two-Wheelers: EV share 6.54%, with March at 9.79%

- Commercial Vehicles: EV share nearly doubled to 1.83% for FY26, March at 2.40%

- Total EV Retail: 24.52 lakh units (+24.63%)

- CNG Vehicles: PV CNG share in March at 23.76%, CV CNG steady at 11.79%

Rising fuel prices have accelerated rather than dampened the transition toward cleaner powertrains.

Urban-Rural Demand Trends

Rural retail grew 13.05% against 13.62% in urban markets, narrowing the gap. Rural demand in PVs outpaced urban at 17.12% versus 10.43%, and March growth showed rural retail at 26.49% versus 23.82% in urban areas.

OEM Market Shifts

Passenger Vehicles:

- Maruti Suzuki: 39.71% share

- Mahindra & Mahindra: 13.42% (second place)

- Tata Motors: 13.04%

- Hyundai: 12.29%

- Toyota Kirloskar: 7.13%

- Kia: 5.94%

Two-Wheelers:

- Hero MotoCorp: 28.40%

- Honda: 25.03%

- TVS: 18.89%

- Royal Enfield: 5.18%

- Ola Electric: 0.77%, Ather Energy: 1.12%

Commercial Vehicles:

- Tata Motors: 34.16%

- Mahindra: 28.11%

- Ashok Leyland: 17.87%

March saw notable shifts with Tata Motors rising to second place in PVs at 14.95%, ahead of Mahindra at 13.87%.

Conclusion

FY26 marked a year of vindication for India’s auto retail market. Policy interventions, improved macroeconomic conditions, and growing consumer confidence combined to deliver record volumes across five of six segments. The stage is set for continued structural expansion in FY27, with electric and CNG adoption deepening across vehicle categories.